RCCN WeChat QrCode

RCCN WeChat QrCode Mobile WebSite

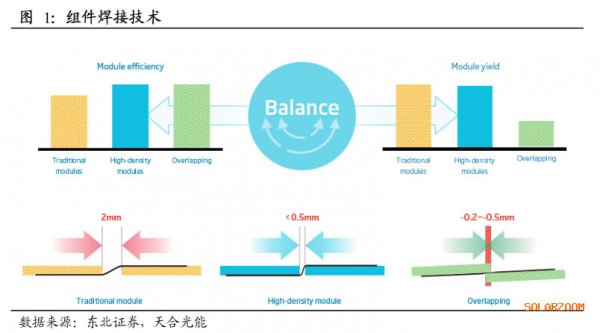

Mobile WebSite1. Iterative power acceleration, comprehensive application of new component technologies

Module power Before the PERC battery was fully popularized in 2018, the single-chip power of 72 modules improved at a rate of about 5 watts per year. Although each new module process has reserves, in actual shipments, it is still single crystal, Flat solder ribbons, 4-5 main grids, and 156mm silicon wafers are the main products. The conventional monocrystalline and polycrystalline silicon wafer technologies are in parallel, and the single crystal penetration rate is steadily increasing.

The continuous technological progress and cost reduction of the photovoltaic silicon industry chain have driven the cost of components to decline steadily. However, when the epidemic affects demand, the price of components delivered in the second half of 2020 has dropped below 1.5 yuan/W, a 20% decrease from the beginning of the year. From the perspective of the industry chain price, the price drop in the upstream link is leading the decline in the component price, and the component delivery price is still falling slightly, but the price in the upstream link has stabilized. After the wave of price cuts, the upstream link has limited room to continue to cut prices. The gross profit margin of companies with the best silicon material cost has been reduced to below 30%. The industry’s profitable production capacity is less than half. The battery price was not profitable in the whole industry from April to May, and the price has stabilized and recovered. Therefore, the absolute cost reduction space of the silicon industry chain in the component cost is already limited. At present, the battery cost accounts for only about 50% of the component cost. Subsequent component cost reductions rely more on battery efficiency and the increase of single module power.